‘When I go on dating apps, I’m looking for an investor, not a husband,’ laughs Juliette*, 36.

The PR exec is single and lives in London. She says her dreams of owning a home in the city will never be a reality unless she couples up.

‘It’s not a position I ever thought I’d be in,’ she admits. ‘I was in a relationship for the latter half of my 20s, and I was saving too.

‘I thought if he matched what I had, that’s a house deposit.

‘But when we split up, it was back to the drawing board. I’ve got about £15,000 saved up, but I probably need to save at least another £15,000 before I can consider buying – even then, I’d only be able to afford a one-bed flat.’

And building up a nest egg isn’t easy. ‘London living is expensive,’ says Juliette. ‘Just transport alone is around £200 a month, and my rent is £800.

‘I could make more sacrifices but people forget when you’re single that if you don’t make plans and arrange to do things with friends, you end up sitting at home alone.

‘Yes, I could move further out, but I don’t know anyone in the likes of Croydon or Essex and when you’re a single, that would make for quite a lonely existence.’

For now, Juliette says she feels trapped, and finds house sharing in her 30s embarrassing – it’s why she chose to be anonymous for this article. ‘It’s a little humiliating,’ she says.

‘Why am I still having arguments with housemates about heating bills and cleaning, as though I’m a student?

‘And telling guys on dates that I still live in a house share makes me cringe.

‘I look at my coupled-up friends, and they’re upsizing. I find it hard to congratulate them. They don’t appreciate how simply being in a relationship has made their situation so much easier.’

There are millions of single people in the UK in Juliette’s position – but as ever, women are being hit the hardest.

The Women’s Budget Group (WBG), a feminist think tank, told Metro that the earnings gap where women take home 29% less than men means home ownership isn’t an option for many.

Their findings make for bleak reading. According to WBG research, shared with Metro, women need over 11 times their annual salaries to be able to buy a home in England, while men need just over eight times.

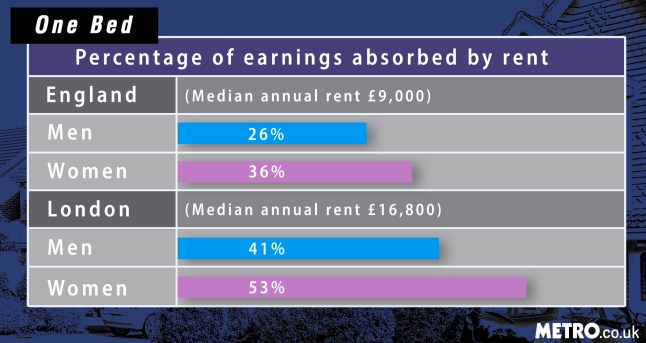

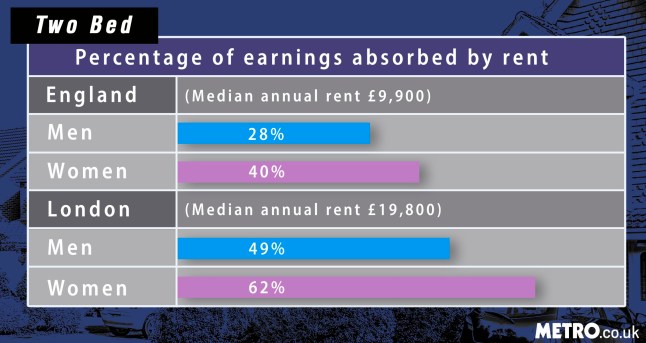

In England, for a one-bedroom property, 36% of women’s median earnings are absorbed by rent, compared to 26% of men’s. This goes up to 53% for women in London and 41% for men respectively.

Dr Mary-Ann Stephenson, director of WBG, told Metro: ‘We know that women are more likely to work part-time, and in sectors that don’t offer bonuses or pay for working extra hours.

‘We also know that women tend to have less savings than men, and are also more likely to get into debt in order to afford day-to-day spending.

‘This all means that they’re far less likely to have money saved up for a house deposit.’

Likewise, data from Fairview Homes shows that women are 68% less confident that they’ll be able to purchase their own home in the next two years than men (53%). Women are also statistically less likely to buy a home with a friend than men – 23% compared with 36%.

Meanwhile, figures from Mojo Mortgages find that women need to save nearly four times as long as men to afford a deposit for their first home. Their analysis of ONS data shows that, on average, men earn £422 more each month after tax, and can save up to 40% more each month.

Research also shows that 90% of single parents are women. Dr Mary-Ann continues: ‘If you’re a single parent, you’re significantly more likely to be in poverty.

‘You have less flexibility at work because you have to be present for things like school pick ups and drop off.

‘Single parents also need bigger homes, because they need rooms for their children – which again, affects affordability.’

And even if you do get onto that first rung of the property ladder, solo home owning has its struggles.

Currently, people living alone in England, Scotland and Wales can claim a 25% discount on their council tax – meaning they still pay 75%. But if two adults (or more) live together, they can of course split it 50/50 between them. This means that people living alone pay an extra £516.24 per year.

Hayley Johnston, 32, owns a home in Northamptonshire. She knows all too well the highs – and lows – of shouldering the burden alone.

She tells Metro: ‘I used a Help to Buy scheme, so I had a 5% deposit of £7,000. There was no way I could have afforded it otherwise! I also lived at home with my parents, so was able to save up.’

She initially paid £450 a month for her mortgage, and says she felt ‘really proud’ to be a homeowner.

But in recent years, Hayley, a teacher, has had to be more careful with her finances. She says: ‘I’ve remortgaged twice and now pay £680 a month.

‘On the surface, I look financially comfortable. I have a house, a gym membership, and a car, but I’m unable to collate any kind of savings. I live pretty much pay cheque to pay cheque.

‘If anyone needed a lump sum or there was some kind of disaster, that’s something I don’t have – I don’t think I’ll be able to have savings until I had a partner.’

However, Hayley says the experience has taught her a lot too.

‘Sometimes I listen to my married friends, and they don’t even know how much their mortgage or bills are. They don’t have a proper overview.

‘The thing about doing this on your own is I’ve learnt a lot about money – I’ve had no other choice!’

While the picture may look bleak for single women, Dr Mary-Ann from WMB says it doesn’t have to be this way.

She explains: ‘We need to make a political choice to build more social housing. The renting market offers no security for long-term letters – they can be evicted quickly.

‘Social housing, owned by associations or local governments, would offer reasonable rents, long-term tenancies and wouldn’t be run for profit.

‘It would see private landlords withdraw, and house prices would go down. It means you wouldn’t need to buy a house to secure a long-term home.

‘The government also needs to invest in early education and childcare, to make it easier for women to work full time, and reduce that earnings gap.’

*Names have been changed

This article was originally published on February 12, 2024.

Do you have a story to share?

Get in touch by emailing MetroLifestyleTeam@Metro.co.uk.